Editor’s note: Glenn Kelman is the CEO of Redfin, a technology-powered real estate broker backed by Madrona Venture Group and Greylock Partners. His last post for TechCrunch was The Maximum, Beautiful Product. Follow him on Twitter @glennkelman.

Silicon Valley home buyers, I wish we had better news. Prices keep rising, with no end in sight.

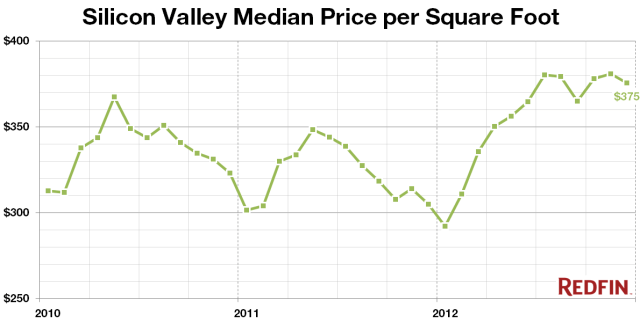

Across the 20 markets Redfin serves, only Phoenix saw more rapid price increases than the Bay Area. Over the last 12 months, San Francisco prices rose 20 percent; San Jose prices jumped 23 percent. When the market moves this fast, the appraisals required by a lender reflect last year’s prices, and sellers just take all-cash deals instead — even when another bidder with a mortgage offers more money. Across California, we are starting to see conventional sales handled more like the sale of foreclosures once were, with the home sold as-is.

What’s going on? Well by December of 2012, the number of homes for sale across the Bay Area had declined 68 percent from the previous year. Once foreclosures stopped flooding the market, there weren’t enough conventional sellers to take their place. Goaded by very low interest rates, buyers turned out in force. High demand and low supply were why we were so bullish in our September TechCrunch assessment of Silicon Valley home prices.

This swing to a seller’s market happened first in California and Arizona, then spread to other parts of the country. Now, the inventory crunch is self-perpetuating, as some homeowners we talk to hesitate to sell for fear they won’t be able to find a place to buy, and even more consider renting out their place instead.

So that’s the recent history of Bay Area real estate. But what’s happening in the market right now, and how is it changing? We’ve noticed four trends:

1. Silent spring: 2013 was the first year in the past six to begin with a broad consensus that home prices were again rising, so we expected the year to start with plenty of new listings.

But in the first two weeks of January, the inventory problem somehow got worse rather than better, with new listings in the Bay Area falling more than 45 percent compared to the same period last year; much of the drop is due to a whopping 72 percent decline in short sales, where the owner sells for less than she owes on the mortgage. When foreclosures first became scarce in 2012, short sales became the preferred way for banks to clear out troubled loans, but with rising prices and more loan modifications, even short sales are now rapidly disappearing.

What this means is that Bay Area real estate is again becoming a free market, where the only people selling are the ones who want to sell. As any East German will tell you, this transition is hard. It’s almost as if homeowners have forgotten how to sell. We expect the supply of homes for sale to increase by the Super Bowl, but if it doesn’t increase a lot, we’re going to have a silent spring, with meager sales gains.

2. Local monopolies: 88 percent of the December offers written by Redfin agents for our Bay Area clients faced competition. Inventory is now so scarce that sellers sometimes enjoy a virtual monopoly, as was the case just last week with a listing that had no competition for half a mile in any direction. Every Redfin agent in the San Francisco office represented a different home-buyer on that property. As Redfin agent Landon Nash likes to say, there’s an enormous difference between competition of any kind and no competition whatsoever; it’s like the difference when raising venture capital between having one term sheet or two.

3. Flash real estate sales: Mobile real estate applications are increasing the pace at which the market moves. After getting listing alerts instantly delivered to their mobile devices, several Redfin clients have been able to get those listings under contract hours later. With so many home-buyers across the Bay Area now getting alerts instantly rather than nightly, the whole home-buying cycle here is becoming more like a flash sale, with properties lasting a day rather than a week.

4. Wild-card offers: As frustration builds among would-be home-buyers, we increasingly see wild-card offers, higher than any competing offer by hundreds of thousands of dollars. According to Brad Le, the leader of Redfin’s Silicon Valley business, “People just get tired of losing, and say, ‘Screw it.’” In just the past few days, a $1.8-million listing in Silicon Valley attracted six offers clustered around a price of $1.95 million, which was at the high end of what recent comparable sales could justify. This kind of competition was familiar to us. But the seventh offer came in half a million dollars higher, at $2.45 million, with no contingencies for an inspection or an appraisal. The seller’s agent was flabbergasted. These are the kinds of shots that send a shiver down the market’s spine.

5. Cash-out buyers: As the U.S. government approached a fiscal cliff, plenty of folks in Silicon Valley with stock in their own companies became worried that capital gains would be taxed at a higher rate, and so rushed to sell their shares by December 31. Redfin saw a spike in the number of high-end customers making an offer on a home in December, and still Redfin agents are representing a handful of clients who cashed out their equity positions with an eye toward using that money to pay for a home. Even as investors become more cautious in the face of increased competition, more cash buyers than ever are entering the market, loaded for bear.

Where will it all end? The truth is, alone among the 20 markets Redfin serves, the Bay Area market is the one I dread getting asked about. Everywhere else follows rational economic laws. But here it just gets crazier and crazier.

[Image via Redfin]